Categories

About UsHow to get startedAccount AccessBrokers and TradingScannersResearch ToolsCommunityStocksOptionsFuturesAlertsVolume Weighted Average Price (VWAP) - Indicator Formula

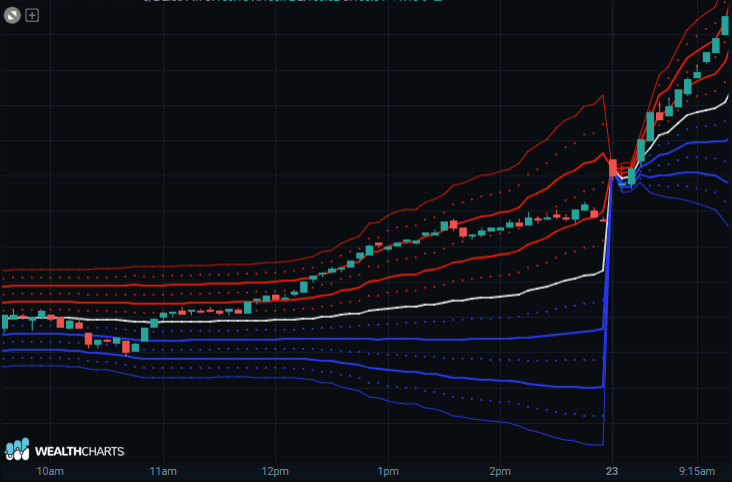

The Volume Weighted Average Price (VWAP) is a measure that represents the weighted average price at which trades of a given time period on a given stock have taken place. The measure is used by institutional investors in particular as a reference for the execution of a purchase and sale operation based on several exchanges.

The vwap and its superior standard deviations and below represent supports and resistances (with particular emphasis on the 2nd band).

On a day in range, strong hands love to buy on weakness (2nd band) and sell on strength (vwap), The price will bounce between vwap and bands. On a strong trend day, the price will come out of the bands.

The same concept can be applied to longer time frames, hence the need to have an indicator on a weekly/month/composite basis. The advantage of the Vwap is that it is always the same in any time frame so you all look at the same thing.